Article

Identity Continuity Is the Only Authentication Architecture Built for the Future

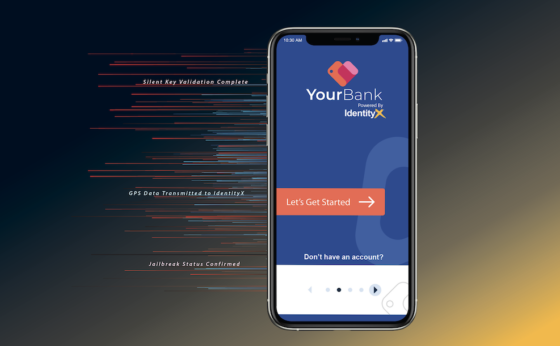

Passwords, security questions, and device-based biometrics were built for a threat landscape that no longer exists. Identity Continuity was built for this one.

Fall 2021">

Fall 2021">

You Verify">

You Verify">